A global recession is looming, and it won’t just be blue-collar workers struggling to keep the wolf from the door. In fact, white-collar workers are much more likely to be under pressure this time1, leading to some potentially awkward conversations with customers who may find themselves in debt for the first time in their lives.

Most companies have customers that owe money occasionally, and there are various ways to retrieve it. In the past, the focus for debt collection was on the cost of retrieval and the success rate. But at a time where company brands and behaviours are under increasing public scrutiny, and new customers are both expensive to find and in short supply, businesses are reviewing the old debt collection model with an eye on the customer’s lifetime value.

In the past, companies have tended to view chasing debt as a solitary function, leading to limited strategies that focus on the best way to recover as much of the debt as possible for the least amount of money. But nowadays a more holistic approach is available for companies who choose to chase the debt themselves, and businesses can now ask better questions, such as “How do we retain customers in debt who are likely to remain valuable to us in the future?”

Using proactive conversational AI, businesses are now able to set more ambitious goals for debt collection than ever, while simultaneously achieving higher rates of return than non-AI alternatives.

It ain’t what you do (It’s the way that you do it)

Increasingly, companies are realising that chasing debt is an opportunity, if done right. Most customers in debt do not begrudge companies chasing what is rightfully theirs. But debt collection can often feel impersonal, heavy-handed, and can create hostile environments where customers feel they are being attacked by the very company they chose to buy from. The message of ‘we care about our customers’ can ring rather hollow as a final-notice red letter from a third-party company gets posted through your front door on behalf of that caring company.

But it appears that a little conversation goes a long way.

With proactive conversational AI, the options for pursuing the long-term relationship strategy over short-term debt retrieval are growing, even when the relationship looks doomed. And the low cost of AI communication tools frees up call centres and in-house departments to focus on high value conversations, opening up the doors for a range of proactive strategies.

Let’s say you run a business and have 500 accounts in arrears of less than $100 each. Let’s also say that those customers typically spend $500/year, and your average customer lifespan is 10 years.

Do you really want to chase the $100 and maybe lose them forever in the process? Could you instead maybe work with the customer to keep them on for those much more valuable 10 years of $500 while still completing the debt recovery process?

In the past, the simple answer would be no. It’s too expensive to spend time managing individual issues relating to low levels of debt. But as companies store more data about their customers, that data can be used in conjunction with AI technology to create ways to find out what the issue is, and what solutions are available, all at low cost.

The new debt collection process

Generally, debt can be categorised into three – someone has a debt that they don’t know about, so didn’t pay; someone had a debt they did know about, but won’t pay, or they knew about the debt, and can’t pay right now.

AI can be adopted to reach out to these customers to establish which of the three categories they fit into.

Let’s take this $100 customer debt as an example. You might use ContactEngine to initiate dialogue with your 500 debtors via SMS— or whichever channel your customer prefers — in seconds. It’s a nice message, because you’re a nice company, and you understand that your brand is as relevant when you are chasing debt as when you are chasing a new customer.

So, it turns out that about a third of your 500 debtors had either moved house, changed email addresses or simply did not get any correspondence, so were surprised to get the text saying they had a debt. But because you sent that nice text, not a legalistic letter in bold writing, your customer is not aggrieved — after all, you’re only asking them to pay for something they thought they had paid for. AI can even provide them payment information to settle the debt immediately.

What about the debtors who did know they were in debt, but can’t pay right now? Well, AI technology can also establish this quickly and effectively, and then send relevant choices for the customer to consider. A lot of customers don’t proactively reach out to companies when they can’t pay debt – the more typical human reaction is to bury one’s head in the sand. If the company initiates contact though, and offers up solutions such as considering partial payment, or a move to direct debit, or a reduction of future services until the debt is paid in full, then the outcomes for recovering debt that cannot be paid as per the original contract improve greatly.

And the third category? Well, if your customer was aware that they had a debt, and can pay it, but won’t, then it may be time to review the relationship with a human agent trained in objection handling. But before the company reaches that point, AI has already established a communication line with the customer, and established that they sit in this third category, allowing the human agent to concentrate on the debt collection process, rather than the admin of finding the person and finding out what the problem is. Or the company can decide that the cost of retrieving this debt may not be worth it, so they can instead write it off, or outsource it to a third-party collector, safe in the knowledge that they have not handed over valuable customers from the first two categories that could be considered valuable ‘low-hanging fruit’.

Within just seven days of initial contact, Proactive AI conversations typically led to:

a) Increases in the collection of accurate contact details, making the debt collection process less likely to occur again, saving operational costs

b) The debt being recovered quicker, increasing cash flow

c) The customer relationship remaining intact, and sometimes healthier than it was before the interaction, increasing the likelihood of long-term customer loyalty

New technology has created better outcomes. The client and customer both have what they want, continue to work together, and are less likely to suffer administrative issues going forward.

Companies are increasingly using AI-led conversations in debt collection to control the tone, frequency and timing of dialogue, the method of communication, and the message itself, while typically securing a higher percentage of the debt.

Perhaps ironically, given the interaction utilises AI, the experience feels more human, and can leave the customer with a positive memory, and a lesson that even in matters of debt, the company they chose still puts them first, by listening and responding to their personal circumstances.

More money, fewer problems

Around two-thirds of contact attempts to retrieve debt are done via letters or manual phone calls, even though 73% of those customers in debt make payments when contacted through digital channels.2 Companies using traditional methods of communication are aware of the need to transition to digital channels such as SMS, email, or DMs because their customers prefer to use these methods of communication. But the quantitative financial gains are also emerging, as proactive conversational AI companies team up with service providers to test real-life scenarios.

ContactEngine was deployed by a leading North American Communications Service Provider to explore a question; If 73% of customers in late delinquency made a payment when contacted through digital channels, how many of those individuals would never have reached late delinquency had their customer journey been automated via the channel of their choice?

ContactEngine provided customers in collection with:

- A streamlined, integrated communication feedback loop that delivers real-time payment information

- Tokenized URLs for instant access to the customer's portal

- Automated in-channel payments with access to stored payment profiles allowing for immediate payment

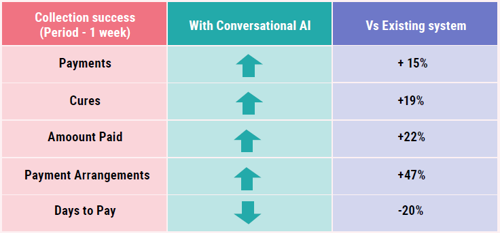

As well as a 47% increase in payment arrangements negotiated, the use of ContactEngine’s AI technology led to a 20% reduction in days waiting to pay, and a 22pc increase in dollar collections, all in one week.